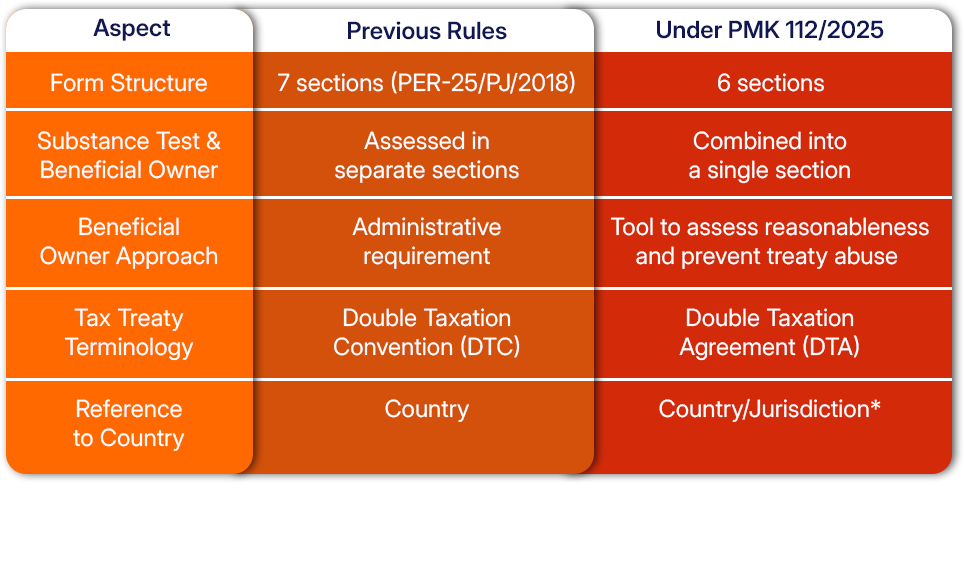

The Indonesian government issued PMK No. 112/2025, effective on 30 December 2025, in accordance with PP No. 55 of 2022 and replaces the previous framework under PER-25/PJ/2018.

PMK 112/2025 introduces changes to the procedures for applying tax treaty benefits, including revisions to the DGT Form, a different approach to assessing beneficial ownership, and adjustments to related administrative processes. These changes are particularly relevant for Indonesian companies that act as withholding agents in cross-border transactions.

Below is an overview of the key changes introduced under PMK 112/2025.

CHANGES IN THE DGT FORM

The document used to claim tax treaty benefits, previously known as the Certificate of Domicile of Non-Resident for Indonesia Withholding Tax, is now referred to as the DGT Form. PMK 112/2025 revises both the structure and content of this form.

* The use of the term Country/Jurisdiction reflects the fact that Indonesia’s tax treaty partners may include jurisdictions that are not fully sovereign states but have their own tax systems.

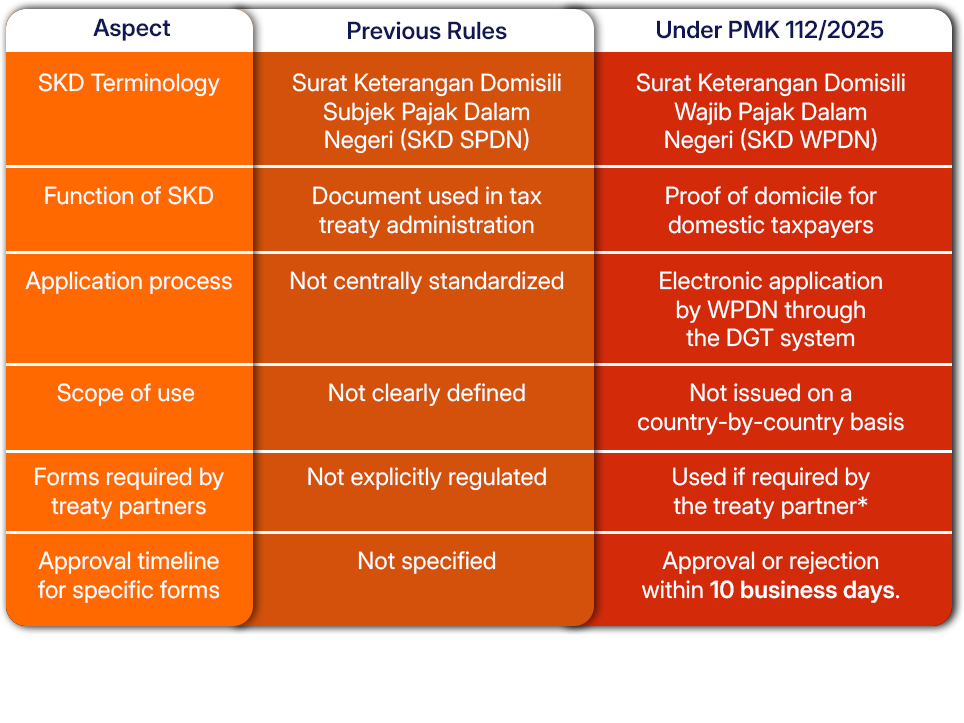

ADMINISTRATIVE CHANGES OUTSIDE THE DGT FORM

In addition to changes to the DGT Form, PMK 112/2025 also updates administrative provisions related to the Certificate of Domicile (SKD) in the context of tax treaty implementation.

*SKD WPDN serves as proof of domicile for domestic taxpayers. Where a treaty partner requires additional or specific forms, such documents are submitted together with the SKD WPDN.

*SKD WPDN serves as proof of domicile for domestic taxpayers. Where a treaty partner requires additional or specific forms, such documents are submitted together with the SKD WPDN.

IMPACT OF PMK 112/2025 ON INDONESIAN COMPANIES

- Tax treaty application is no longer purely administrative

Treaty benefits must reflect the substance of the transaction and the underlying business arrangement. - Greater responsibility for withholding agents

Companies must ensure that the DGT Form and related documents are valid and applicable at the time withholding tax is imposed. - Higher risk of adjustments in case of inconsistencies

Any mismatch between documentation, transaction substance, and document validity may result in the denial of treaty benefits during a tax audit.

PMK 112/2025 marks a shift in Indonesia’s approach to tax treaty implementation, moving from a largely administrative focus to a greater emphasis on substance and transaction reasonableness. Companies should review their internal policies, documentation, and cross-border transaction processes to align with the updated requirements.

NEED ASSISTANCE IN NAVIGATING THE NEW TAX TREATY RULES UNDER PMK 112/2025?

Moores Rowland Indonesia provides tax services covering tax treaty reviews, withholding tax risk analysis, and cross-border tax compliance to help companies manage risks and ensure accurate tax treatment.